As we move through 2026, the battle for the “Best Small-to-Midsize Business (SMB) Retirement Plan” has narrowed down to two giants: Fidelity Investments and Charles Schwab.

With the 2026 updates to the SECURE 2.0 Act now in full effect—including mandatory auto-enrollment for new plans and increased “catch-up” contributions for employees aged 60–63—business owners face a complex decision. Choosing between Fidelity and Schwab isn’t just about “low fees”; it’s about integration with your payroll, ease of IRS reporting, and the quality of the investment menu you provide to your employees.

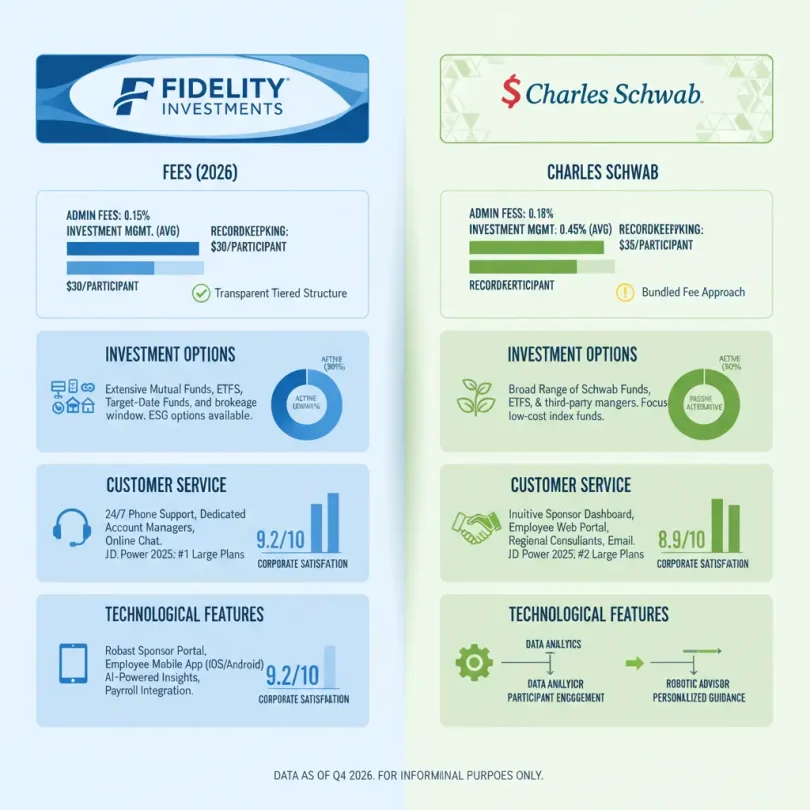

1. Fidelity: The Institutional Retirement Heavyweight

Fidelity is the largest provider of 401(k) plans in the United States. In 2026, they have leveraged this scale to offer a “holistic” benefit ecosystem.

- The 2026 Advantage: Fidelity’s NetBenefits® platform is the gold standard for employee experience. It allows workers to see their 401(k), HSA, and stock options in a single view.

- Investment Selection: Fidelity offers its “Zero” expense ratio funds, which are a massive selling point for plan sponsors looking to minimize the “fiduciary drag” on employee returns.

- Solo 401(k) for Founders: For 2026, Fidelity’s Self-Employed 401(k) now supports Roth contributions natively, making it a top pick for high-earning freelancers.

- Best For: Companies looking for a “set it and forget it” solution with world-class employee education and planning tools.

2. Charles Schwab: The Flexibility and Simplicity Leader

Schwab has positioned itself in 2026 as the more “user-friendly” and flexible alternative for growing startups and professional service firms.

- The 2026 Advantage: Schwab’s Index Advantage® plan is specifically designed to keep costs low by using institutional-grade index funds. In 2026, they have significantly improved their automated 401(k) administration, reducing the paperwork burden for small business owners.

- Brokerage Link: Schwab remains the leader for “Self-Directed” employees. Through “BrokerageLink,” employees can move a portion of their 401(k) into a brokerage account to trade individual stocks or ETFs—a feature many tech-savvy employees demand in 2026.

- Integration: Schwab has better native integration with third-party payroll providers like Gusto and Rippling compared to Fidelity’s more proprietary approach.

- Best For: Startups and firms with sophisticated employees who want more control over their investment choices.

3. Key Comparison: 2026 Small Business Features

| Feature | Fidelity (SMB 401k) | Charles Schwab (Index Advantage) |

| Setup Fees | Generally $0 (varies by size) | Generally $0 (varies by size) |

| Employee Experience | Industry-leading (NetBenefits) | Highly intuitive & simple |

| Investment Style | Strong focus on Mutual Funds | Strong focus on ETFs & Index Funds |

| Self-Directed Option | Available (Limited) | Best-in-Class (BrokerageLink) |

| Crypto Access | Yes (Fidelity Crypto) | No (ETF-only) |

4. The 2026 SECURE 2.0 Compliance Check

Both firms have updated their platforms for 2026 to handle the latest IRS requirements. If you are starting a plan this year, you must ensure your provider handles:

- Automatic Enrollment: New plans (post-2025) must automatically enroll employees at a rate of 3% to 10%.

- Higher Catch-up Limits: For 2026, the catch-up limit for employees aged 60, 61, 62, and 63 has increased to $11,250 (up from $7,500 in previous years).

- Roth SIMPLE IRAs: If you choose a SIMPLE IRA instead of a 401(k), 2026 is the first year both Fidelity and Schwab fully support employer-contributed Roth options.

5. Pricing and Fiduciary Responsibility

A major change in 2026 is the increased scrutiny on Plan Sponsor Fiduciary Liability.

- Schwab tends to be more transparent with its “all-in” fee structures, making it easier for a small business owner to prove they are acting in the employees’ best interests.

- Fidelity offers deeper “Fiduciary Support Services,” where they take on more of the legal responsibility for investment selection, though this often comes with a higher administrative cost for the employer.