Choosing someone to manage your hard-earned money is one of the most significant financial decisions you’ll ever make. This isn’t just about picking an advisor; it’s about finding a long-term partner who will help you navigate complex markets, plan for your future, and protect your legacy. For residents of [City, State], finding a local, trustworthy wealth manager who understands the unique financial landscape is crucial. But with so many options, how do you separate the best from the rest?

A seasoned financial professional once shared a startling perspective. When asked what percentage of financial advisors he would recommend to his own mother, his answer was a mere “two percent.” Why so few? He explained that while many advisors possess one or two essential qualities, very few have the complete trifecta of expertise, trustworthiness, and genuine care.

This guide is designed to help you find an advisor in that top two percent. We will walk you through the essential qualities of a trustworthy wealth manager, provide a step-by-step process for finding one near you in [City, State], and highlight the red flags to avoid. By the end, you’ll be equipped with the knowledge to confidently choose a financial partner who can help turn your financial goals into reality.

What Makes a Wealth Manager Trustworthy?

A trustworthy wealth manager is more than just a stock picker. They are a comprehensive financial guide who aligns their strategies with your life goals. When evaluating potential advisors, focus on a combination of their professional qualifications and personal character.

Qualities to Look For

The best financial advisors share three core qualities that set them apart. These are the non-negotiables you should look for in any professional you hire, especially one managing your wealth.

- Expertise in Your Area of Need: Financial management is not one-size-fits-all. A young professional growing their portfolio has vastly different needs than a business owner planning for succession or a family preparing for retirement. You need an advisor who specializes in your specific financial situation. For example, a wealth manager with a proven track record in guiding families in [City, State] through complex estate planning can offer invaluable local insights that a generalist cannot. Look for someone with at least five years of experience, as they will have navigated both bull and bear markets and can offer seasoned guidance.

- Unquestionable Trustworthiness: Trust is the bedrock of any successful client-advisor relationship. A trustworthy advisor is transparent, honest, and always puts your interests first. They should be upfront about their fee structure, potential conflicts of interest, and the risks associated with any investment strategy. If an advisor only presents the positives and glosses over the downsides, consider it a major red flag. True professionals will give you a balanced view, preparing you for all potential outcomes.

- Genuine Care for Your Success: Does the advisor seem genuinely interested in you, your family, and your aspirations? A caring advisor takes the time to understand your unique circumstances before offering any advice. They should ask thoughtful questions about your long-term goals and be committed to building a lasting relationship. The initial meetings should feel less like a sales pitch and more like the beginning of a partnership. Trust your intuition; if you feel a sincere connection and sense that they are invested in your success, it’s a positive sign.

Certifications and Credentials

Professional designations are a clear indicator of an advisor’s commitment to their field. They signify a high level of expertise and adherence to strict ethical standards. When searching for a wealth manager in [City, State], look for these key credentials:

- CERTIFIED FINANCIAL PLANNER™ (CFP®): This is one of the most respected certifications in the industry. CFP® professionals have completed rigorous coursework, passed a comprehensive exam, and must meet ongoing education requirements. They are also held to a fiduciary standard, meaning they must act in their client’s best interest.

- Certified Public Accountant/Personal Financial Specialist (CPA/PFS): A CPA with a PFS credential combines extensive tax knowledge with financial planning expertise. This is particularly valuable for business owners and high-net-worth individuals looking to optimize their financial strategies for tax efficiency.

- Chartered Financial Analyst (CFA®): The CFA charter is a globally recognized standard for investment professionals. It demonstrates deep expertise in investment analysis, portfolio management, and wealth management.

These credentials, combined with a relevant educational background like a degree in finance, business, or accounting, provide a strong foundation of expertise.

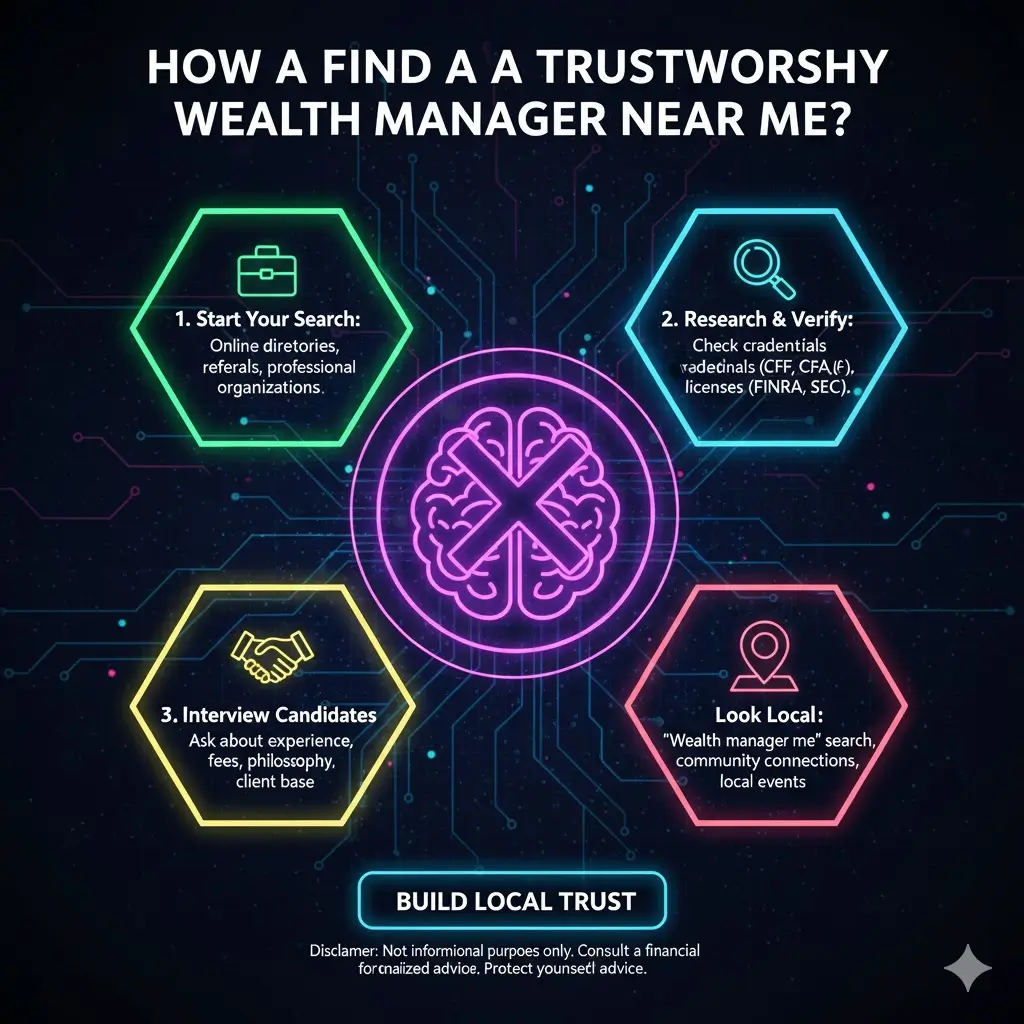

How to Find a Wealth Manager in [City, State]

Finding the right wealth manager is a systematic process. Follow these steps to identify and vet potential candidates to ensure you find a trustworthy partner.

Step 1: Research and Create a List

Start by compiling a list of potential wealth managers in the [City, State] area. Leverage both online and local resources:

- Local Referrals: Ask friends, family, or colleagues for recommendations. A personal endorsement from someone you trust can be a powerful starting point.

- Financial Planning Association (FPA): The local FPA chapter in [City, State] can be a great resource for finding qualified and vetted financial planners.

- Online Directories: Websites like NerdWallet and Investopedia offer directories and reviews of financial advisors.

Step 2: Check Credentials and Background

Once you have a shortlist, it’s time to do your homework. Verify each advisor’s credentials and check for any disciplinary history.

- SEC’s IAPD Database: Use the SEC’s Investment Adviser Public Disclosure (IAPD) website to review an advisor’s registration, employment history, and any past disciplinary actions.

- FINRA BrokerCheck: If the advisor is also a broker, you can check their record through FINRA’s BrokerCheck tool.

- [State] Securities Division: Your state’s securities division provides information on registered advisors and can be a valuable resource for verifying credentials and checking for complaints.

Step 3: Read Reviews and Testimonials

Look for client testimonials on the advisor’s website and read reviews on third-party sites like the Better Business Bureau (BBB). While testimonials are often curated, they can still provide insight into the client experience. For instance, stories of how a manager helped a local [City, State] business owner optimize their retirement plan or guided a family through multi-generational wealth transfer can be very telling.

Step an 4: Schedule Initial Consultations

The initial consultation is your opportunity to interview potential advisors. Most trustworthy advisors offer a free initial meeting. Prepare a list of questions to ask, focusing on their experience, investment philosophy, and how they would approach your specific situation. This meeting is as much about assessing their personality and communication style as it is about their expertise. Do they listen more than they talk? Do they explain complex topics in a way you can understand?

Step 5: Understand the Fee Structure

A trustworthy wealth manager will be completely transparent about how they are compensated. It’s essential to understand their fee structure to identify any potential conflicts of interest.

- Fee-Only: These advisors are compensated directly by their clients, typically through a percentage of assets under management (AUM), a flat fee, or an hourly rate. They do not earn commissions, which minimizes conflicts of interest.

- Fee-Based: This is a hybrid model where advisors may charge fees and also earn commissions on certain products. If you consider a fee-based advisor, ask for a detailed breakdown of all potential compensation.

- Commission-Based: These advisors earn money by selling financial products. This model can create a significant conflict ofinterest, as their recommendations may be influenced by the potential commission rather than your best interests.

Always ask for a complete disclosure of all fees in writing. An advisor who is hesitant to discuss their compensation is a major red flag.

Red Flags to Watch Out For

Just as important as knowing what to look for is knowing what to avoid. Be vigilant and watch for these warning signs when evaluating a potential wealth manager.

- Guaranteed Returns: No legitimate wealth manager can guarantee returns. The market is inherently unpredictable, and any promise of surefire profits is a clear sign of a potential scam.

- Aggressive Sales Tactics: A trustworthy advisor will give you time and space to make an informed decision. High-pressure tactics or demands for an immediate commitment are unprofessional and suggest the advisor is more interested in their bottom line than your financial well-being.

- Lack of Transparency: If an advisor is vague about their investment strategies, avoids discussing fees, or is unwilling to disclose potential conflicts of interest, walk away. Transparency is non-negotiable.

- Poor Communication: A good wealth manager is proactive and communicates regularly. If they are difficult to reach or fail to provide clear, consistent updates, it can be a sign of poor service and a lack of care for their clients.

The Role of Technology in Wealth Management

Modern wealth management is increasingly powered by technology. The best advisors leverage advanced tools to enhance their services, provide greater transparency, and deliver a better client experience. Cutting-edge platforms allow for sophisticated portfolio analysis, real-time reporting, and secure client portals where you can monitor your investments. This use of technology not only improves efficiency but also builds trust by giving you a clear view of your financial picture at all times.

The Importance of a Fiduciary Standard

One of the most critical factors in choosing a wealth manager is their commitment to a fiduciary standard.

What Is a Fiduciary?

A fiduciary is a financial advisor who is legally and ethically obligated to act in their client’s best interest at all times. This is the highest standard of care in the financial industry. It means they must put your interests ahead of their own and those of their firm.

Why It Matters

A non-fiduciary advisor is only required to recommend products that are “suitable,” which is a much lower standard. A suitable investment might be appropriate for your risk tolerance, but it may also come with high fees or commissions that benefit the advisor more than you. By contrast, a fiduciary must recommend the most cost-effective and beneficial option for you, even if it means they earn less.

Always ask a potential wealth manager directly, “Are you a fiduciary?” and get their answer in writing. Adherence to the Investment Advisers Act of 1940, along with compliance with SEC and FINRA regulations, is a minimum requirement.

Building a Long-Term Relationship

Finding a trustworthy wealth manager in [City, State] is the first step in a long and hopefully prosperous journey. The goal is to build a lasting partnership based on mutual trust, open communication, and a shared vision for your financial future. A great advisor will grow with you, adapting your financial plan as your life changes, and will be there to guide you through every milestone, from buying a home to planning your estate.

With proactive communication, customized strategies, and a deep understanding of the local [City, State] financial environment, a top-tier wealth manager can provide the confidence and peace of mind you need to achieve your goals.

Ready to take the next step?

[Find a vetted advisor today]

The information provided in this blog post is for informational purposes only and does not constitute financial advice. Consult with a qualified financial advisor for personalized advice.

Investment involves risk, including the potential loss of principal. Past performance is not indicative of future results.

Our firm is not responsible for the advice or services provided by wealth managers or financial advisors listed or mentioned in this blog post. Always conduct your own due diligence.

This blog post may contain affiliate links. We may receive compensation if you click on these links and engage with the linked services, at no cost to you.